Federal Reserve monetary tightening creates an unusual paradigm shift

Video section is only available for

PREMIUM MEMBERS

Economically speaking, we live in a very unusual time in the way economists interpret upbeat economic data. Reports that reveal solid economic advancements in the past have been interpreted in a positive light as suggest economic growth and prosperity.

However, recently there has been a shift or reversal of that paradigm. The paradigm shift that I am addressing is the reaction of market participants and investors to solid economic reports that reveal economic growth.

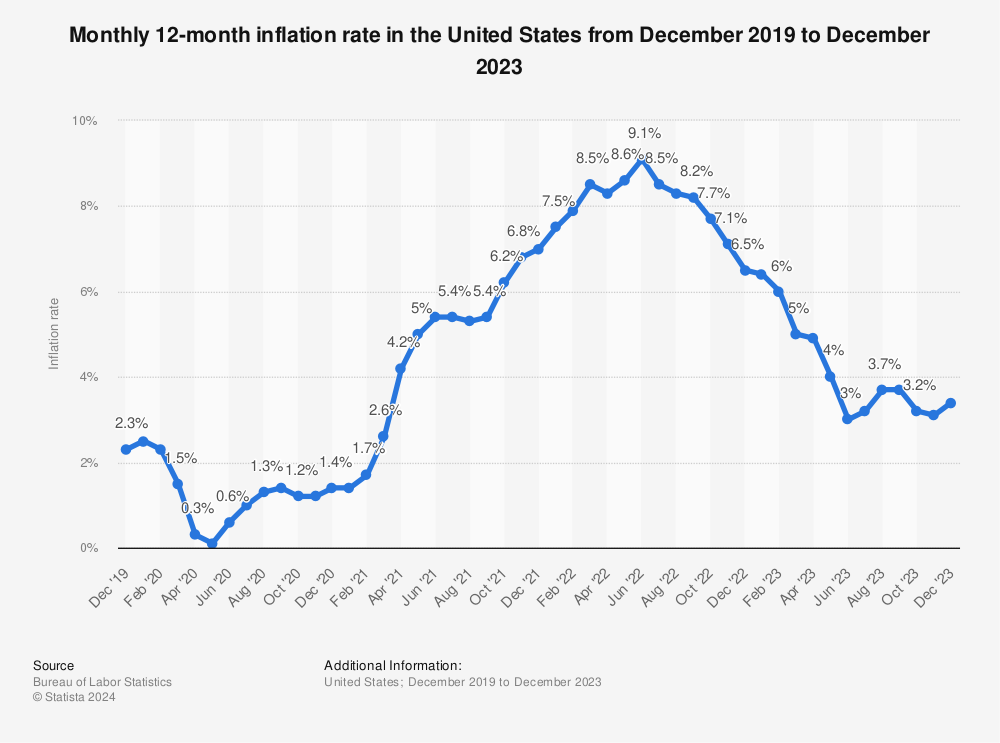

This paradigm shift is a direct result of the Federal Reserve using its monetary policy tools (which primarily include rate hikes) to move inflation closer to its target of 2%. Inflation spiraled tremendously and peaked between March and June 2022. Respectively inflation was running as high as 9.1% and 7% year-over-year, depending if you are looking at headline inflation or core inflation which strips out the volatile price changes in food and energy.

In April 2020 the last thing I consumer’s minds was inflation as it was running below 1% on an annual basis. However, inflation began to slowly move up and by the following year in April 2021, annual inflation was running over double the year prior at 2.6%. Since the Federal Reserve has long maintained a desired target of 2% inflation there was no real reason to focus upon. However, by June 2022 inflation was rising at such a rapid pace it was spiraling out of control and peaked at over 9%. Up until March 2022, The Federal Reserve did not react to spiraling inflation because they assumed that inflation was transitory. They incorrectly assumed that inflation was primarily based upon supply chain issues and other factors suggesting inflation would come back into alignment on its own.

In their brilliance, the Federal Reserve raised rates by ¼% one month before the peak doing too little, too late. The Federal Reserve’s monetary policy was reactive, not proactive.

It was during this period of the Fed’s restrictive monetary policy that the major paradigm shift occurred. The paradigm shift changes the way we view economic growth and its benefits. In other words, economic growth or good news has now become bad news.

An example today is an exceedingly strong jobs report that caused alarm among Federal Reserve officials. Unquestionably, the Federal Reserve is worried about economic reports that show that their restrictive policy cannot always yield economic growth. In other words, good news is bad nad news to the Fed.

For those who would like more information simply use this link.

Wishing you as always good trading,

Gary S. Wagner - Executive Producer